India’s MSME sector plays a critical role in driving exports and sustaining import–export activity, yet access to timely and affordable trade finance has long remained a bottleneck. In this context, the partnership between Drip Capital and YES BANK marks a meaningful shift in how working capital is delivered to small and medium businesses engaged in global trade.

Instead of relying solely on traditional lending models, which often involve lengthy documentation, collateral requirements, and delayed approvals, this collaboration introduces a more streamlined, technology-driven approach. The result is a financing ecosystem that is faster, more flexible, and better aligned with the real cash flow cycles of importers and exporters.

A Shift from Traditional Trade Finance to Digital Lending

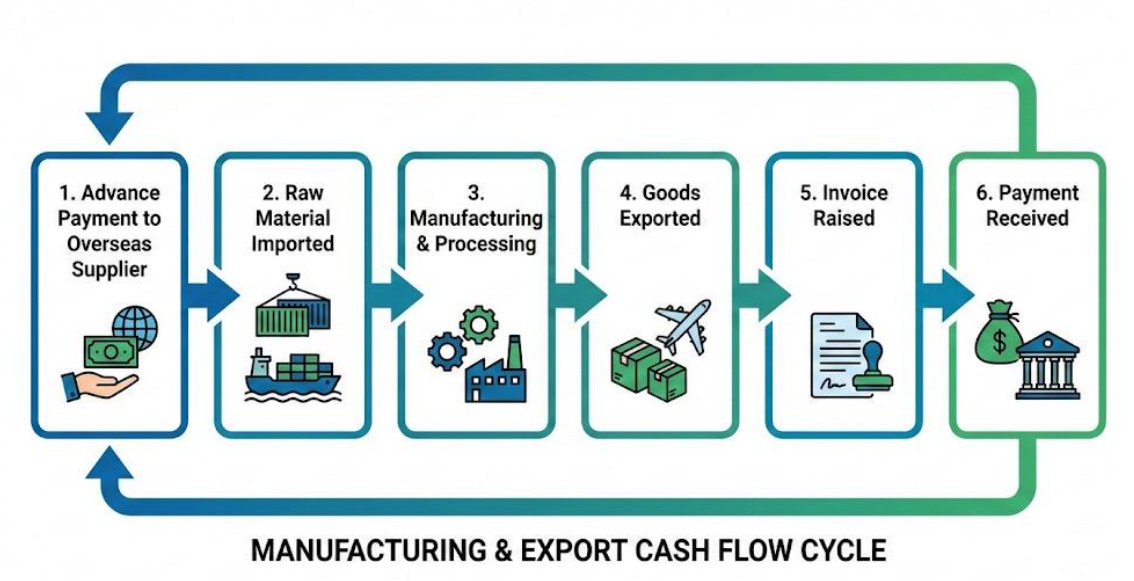

For decades, MSMEs engaged in international trade have struggled with one recurring challenge: the mismatch between payment cycles and operational expenses. Exporters often ship goods and wait 30–90 days (or longer) for payments, while importers must pay suppliers upfront or within short credit windows. This creates constant pressure on working capital.

The Drip Capital–YES BANK partnership addresses this gap by combining fintech-led underwriting with a strong banking backbone. Drip Capital brings digital assessment tools that evaluate creditworthiness quickly, while YES BANK contributes its established financial infrastructure and regulatory strength. Together, they create a hybrid model that reduces friction in the lending process.

This evolution is not just about faster loans-it is about reimagining how trade finance is delivered in a digital-first economy.

How This Impacts Importers and Exporters

For exporters, the biggest advantage lies in improved liquidity. Instead of waiting for buyers to settle invoices, businesses can unlock capital immediately after shipment. This enables them to take on larger orders, expand into new markets, and maintain consistent production cycles without cash flow disruptions.

For importers, the benefits are equally important. Access to structured financing allows them to manage supplier payments more efficiently, negotiate better terms, and avoid delays in procurement cycles. This stability in funding directly translates into more reliable supply chains and smoother inventory planning.

In both cases, MSMEs gain the ability to operate with greater financial predictability, which is essential in global trade where timing often determines profitability.

The Bigger Picture: Strengthening India’s Export Competitiveness

India’s ambition to scale its exports requires a strong foundation of financial accessibility. MSMEs contribute a significant share of India’s export output, but many are constrained not by demand, but by access to credit.

By integrating fintech efficiency with banking reliability, this partnership helps reduce the credit gap in trade finance. It also supports financial inclusion for smaller exporters in tier-2 and tier-3 cities who often find it difficult to meet stringent lending criteria.

Over time, such collaborations can improve India’s position in global supply chains by enabling smaller businesses to compete at international standards of speed, reliability, and scale.

The Role of Technology in Trade Finance Evolution

One of the most important aspects of this development is the role of technology. Traditional lending systems often rely heavily on manual processes and historical financial statements. In contrast, digital trade finance platforms use data-driven underwriting, real-time transaction analysis, and automated risk assessment.

This reduces approval times significantly and makes financing more adaptive to business conditions. As digital adoption increases, we are likely to see trade finance becoming more embedded within export–import platforms, shipping systems, and even accounting software.

The Drip Capital–YES BANK partnership is a step in this direction, where financial services are no longer standalone processes but integrated parts of the trade ecosystem.

Why This Matters Now

Global trade is becoming increasingly competitive, and delays in financing can directly impact market opportunities. For Indian MSMEs, even a few weeks of delayed working capital can mean missed export contracts or strained supplier relationships.

This partnership signals a broader shift in India’s financial ecosystem—toward faster, more inclusive, and technology-enabled credit systems. It reflects how banks and fintech companies are now working together rather than independently to solve structural challenges in trade.

Future Outlook for MSME Trade Finance

The direction is clear: trade finance is becoming more automated, data-driven, and accessible. In the coming years, we are likely to see deeper integration of AI-based credit scoring, real-time shipment-linked financing, and end-to-end digital trade platforms.

For importers and exporters, this means less time spent on paperwork and more time focused on scaling operations, entering new markets, and improving competitiveness. The Drip Capital and YES BANK partnership is more than a financial collaboration-it represents the modernization of trade finance in India. By combining technology with traditional banking strength, it opens new opportunities for MSMEs to access capital faster and more efficiently.

For businesses engaged in import and export, this development is a strong signal that the future of trade finance will be faster, simpler, and far more aligned with real business needs.